With 1.39 million coronavirus cases and 79,382 deaths globally, the world continues to battle the COVID-19 pandemic. Even before the outbreak, the outlook for the world economy—and especially developing countries like Nigeria—was fragile, as global GDP growth was estimated to be only 2.5 percent in 2020. While many developing countries have recorded relatively fewer cases—Nigeria currently has 238 confirmed cases and 5 deaths as of this writing—the weak capacity of health care systems in these countries is likely to exacerbate the pandemic and its impact on their economies.

THE IMPACT ON THE NIGERIAN ECONOMY

Before the pandemic, the Nigerian government had been grappling with weak recovery from the 2014 oil price shock, with GDP growth tapering around 2.3 percent in 2019. In February, the IMF revised the 2020 GDP growth rate from 2.5 percent to 2 percent, as a result of relatively low oil prices and limited fiscal space. Relatedly, the country’s debt profile has been a source of concern for policymakers and development practitioners as the most recent estimate puts the debt service-to-revenue ratio at 60 percent, which is likely to worsen amid the steep decline in revenue associated with falling oil prices. These constraining factors will aggravate the economic impact of the COVID-19 outbreak and make it more difficult for the government to weather the crisis.

AGGREGATE DEMAND WILL FALL, BUT GOVERNMENT EXPENDITURE WILL RISE

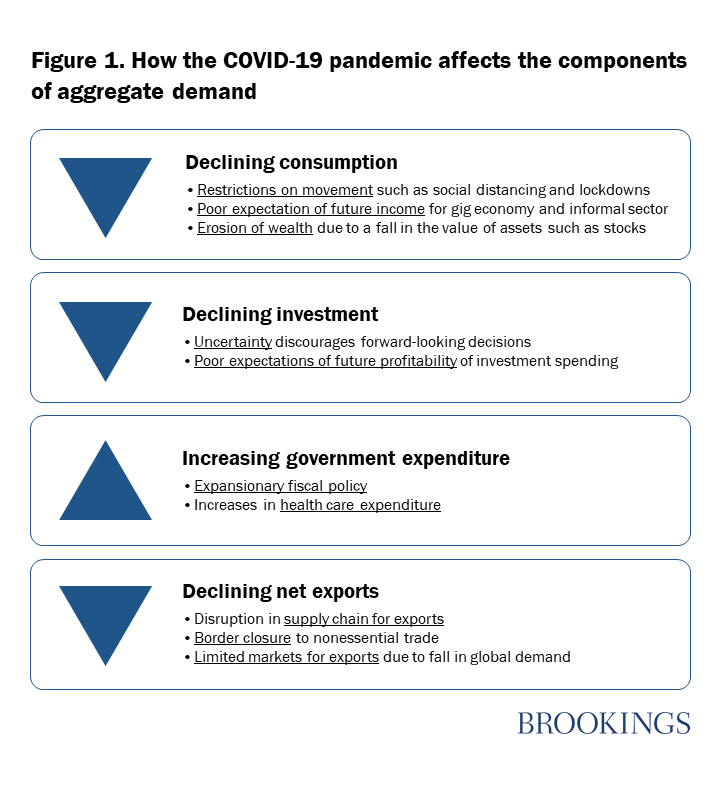

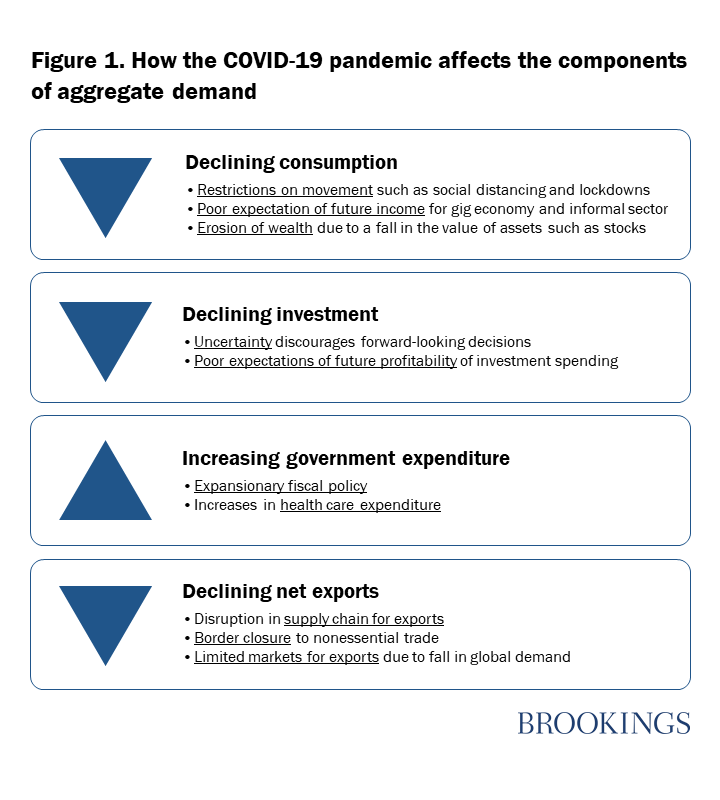

In Nigeria, efforts were already being made to bolster aggregate demand through increased government spending and tax cuts for businesses. The public budget increased from 8.83 trillion naira ($24.53 billion) in 2019 to 10.59 trillion naira ($29.42 billion) in 2020, representing 11 percent of the national GDP, while small businesses have been exempted from company income tax, and the tax rate for medium-sized businesses has been revised downwards from 30 to 20 percent. Unfortunately, the COVID-19 crisis is causing all components of aggregate demand, except for government purchases, to fall (Figure 1).

The fall in household consumption in Nigeria will stem from 1) partial (or full) restrictions on movement, thus causing consumers to spend primarily on essential goods and services; 2) low expectations of future income, particularly by workers in the gig economy that are engaged on a short-term/contract basis, as well as the working poor in the informal economy; and 3) the erosion of wealth and expected wealth as a result of the decline in assets such as stocks and home equity. The federal government has imposed a lockdown in Lagos and Ogun states as well as Abuja (which have the highest number of coronavirus cases combined). Subnational governments have quickly followed suit by imposing lockdowns in their states. Nigeria has a burgeoning gig economy as well as a large informal sector, which contributes 65 percent of its economic output. Movement restrictions have not only reduced the consumption of nonessential commodities in general, but have affected the income-generating capacity of these groups, thus reducing their consumption expenditure.

Investments by firms will be impeded largely due to the uncertainties that come with the pandemic-limited knowledge about the duration of the outbreak, the effectiveness of policy measures, and the reaction of economic agents to these measures—as well as negative investor sentiments, which are causing turbulence in capital markets around the world. Indeed, the crisis has led to a massive decline in stock prices, as the Nigerian Stock Exchange records its worst performance since the 2008 financial crisis, which has eroded the wealth of investors. Taking into consideration the uncertainty that is associated with the pandemic and the negative profit outlook on possible investment projects, firms are likely to hold off on long-term investment decisions.

On the other hand, government purchases will increase as governments, which typically can afford to run budget deficits, utilize fiscal stimulus measures to counteract the fall in consumer spending. However, for governments that are commodity dependent, the fall in the global demand for commodities stemming from the pandemic will significantly increase their fiscal deficits. In Nigeria’s case, the price of Brent crude was just over $26 a barrel on April 2, whereas Nigeria’s budget assumes a price of $57 per barrel and would still have run on a 2.18 trillion naira ($6.05 billion) deficit. Similarly, with oil accounting for 90 percent of Nigeria’s exports, the decline in the demand for oil and oil prices will adversely affect the volume and value of net exports. Indeed, the steep decline in oil prices associated with the pandemic has necessitated that the Nigerian government cut planned expenditure. In fact, on March 18, the minister of finance announced a 1.5 trillion naira ($4.17 billion) cut in nonessential capital spending.

The restrictions on movement of people and border closures foreshadow a decline in exports. Already, countries around the world have closed their borders to nonessential traffic, and global supply chains for exports have been disrupted. Although the exports of countries that devalue their currency due to the fall in the price of commodities (like Nigeria), will become more affordable, the limited markets for nonessential goods and services nullifies the envisaged positive effect on net exports.

WHAT ARE THE POLICY RESPONSES BY THE NIGERIAN GOVERNMENT?

Already, the Central Bank of Nigeria (CBN) has arranged a fiscal stimulus package, including a 50 billion naira ($138.89 million) credit facility to households and small and medium enterprises most affected by the pandemic, a 100 billion naira ($277.78 million) loan to the health sector, and a 1 trillion naira ($2.78 billion) to the manufacturing sector. In addition, the interest rates on all CBN interventions have been revised downwards from 9 to 5 percent, and a one-year moratorium on CBN intervention facilities has been introduced, effective March 1.

With oil being Nigeria’s major source of foreign exchange, amid the steep decline in oil prices, the official exchange rate has been adjusted from 306 to 360 naira. The exchange rate under the investors and exporters (I&E) window has also been adjusted from 360 to 380 naira in order to unify the exchange rates across the I&E window, Bureau de Change, and retail and wholesale windows. Furthermore, the government has introduced import duty waivers for pharmaceutical companies and increased efforts toward ensuring that they receive forex.

WHAT OTHER POLICY RESPONSES CAN BE IMPLEMENTED?

Given the size and scope of the economic impact of the pandemic, there is the need to implement other recovery strategies to stimulate demand. Thus, we recommend the following fiscal and monetary policy measures:

- Although there is a cash transfer program in place, the federal government should improve efforts towards enhancing the efficiency and effectiveness of the distributive mechanisms to reach households that are worst-hit by the pandemic.

- The Federal Inland Revenue Service (FIRS) as well as State Inland Revenue Services (SIRS) should waive payments on personal and corporate income tax for the second quarter of 2020, considering that the shock has affected the income and profits of households and businesses.

- The CBN’s decision to increase the cash reserve ratio (CRR) from 22.5 percent to 27.5 percent in January 2020 should be revisited to provide liquidity for banks so that banks can, in turn, create credit to the private sector.

- FIRS and SIRS should delay tax collection for the worse-hit sectors including tourism, the airline industry, and hoteliers in order to enable them recover from the steep decline in demand.

- To provide additional liquidity in the forex market, the CBN should establish a swap facility with the U.S. Federal Reserve and/or the People’s Bank of China, as was done in 2018, to provide dollar and yen liquidity to financial institutions, investors, and exporters. This move would ease up forex shortage in the financial market and economy.

- While the naira has been adjusted as a result of the forex shortage, it is important that the CBN maintains exchange rate stability by deploying external reserves in order to avoid investors selling off naira-denominated assets.

The COVID-19 pandemic is a wake-up call to policymakers as the unusual and unprecedented nature of the crisis has made it impossible for citizens to rely on foreign health care services and more difficult to solicit for international support given the competing demand for medical supplies and equipment. A more integrated response spanning several sectors—including the health, finance, and trade sectors—is required to address structural issues that make the country less resilient to shocks and limit its range of policy responses. In the long term, tougher decisions need to be made, including but not limited to diversifying the country’s revenue base away from oil exports and improving investments in the health care sector in ensuring that the economy is able to recover quickly from difficult conditions in the future.

This article was first published at Brookings.edu

{kind=link}