Nigeria’s power sector was unbundled and partially privatized to establish a competitive market intended to improve management and efficiency, attract private investment, increase generation, and provide reliable and cost-efficient power supply. However, five years later:

- Operational generation capacity has dropped by 33 percent

- Only 23 percent of the cost of electricity production is recovered1

- Revenue has fallen by 85 percent

Primary Challenges

- Flawed Privatization Model: Expectations were overly-optimistic. Erroneous assumptions included revenue-sufficient tariffs, stable transmission infrastructure; an efficient bulk trader; government institutions would pay their electricity bills, and that the DisCos would be financial viability. The bidding process often penalised or eliminated conservative bidders with more realistic analyses.

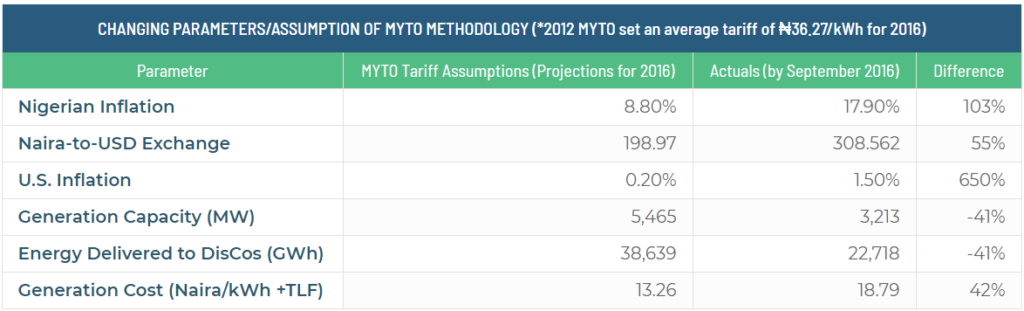

- Low Electricity Pricing: The Multi-Year Tariff Order (MYTO) became too low to cover costs due after insufficiently accounting for increasing costs of generation and gas, and a weakening exchange rate for the naira. Cost recovery, and therefore return on investment, became impossible.2

- Gas Supply Shortage: Post-privatization GenCos depended on gas for 80 percent of grid capacity, but gas infrastructure is weak, suffers from vandalism, and is vulnerable to Niger-Delta militancy.3 Major capacity shortfalls followed.4

- Liquidity Crisis: With GenCos and DisCos unable to recover costs, they were then unable to repay the $780 million borrowed from Nigerian banks for the initial purchase.5,6 Subsequently, the banks have been unwilling to provide further loans to GenCos and DisCos that would allow for investment in infrastructure improvements.

Achievements: Nonetheless some milestones have been achieved since privatization including:

- Increase in installed capacity for power generation;

- Expansion of the transmission network;

- Some roll out of meters and modest progress to boost utility revenues;

- Greater demand for power sector equipment that led to private sector investments and participation across the value chain.

Way Forward: To ensure sustainability and minimize debt accumulation across the value chain, Nigeria may need to:7

- Implement a true cost-reflective tariff to encourage more efficient service delivery and enable cost recovery for the investors in the sector.

- Sell some government shares to raise capital and take steps to attract new investors.

- Bolster the distribution network by expanding metering, completing customer and asset enumeration, and conducting energy demand studies.

- Reform the gas sector by adjusting gas prices to be cost-reflective, clearing outstanding debts to suppliers, signing pending supply and transportation agreement, and reinforcing risk mitigation requirements and gas supply commitments.

Endnotes

- Nextier Power (2018), “The Aftermath: Moving Forward”

- Premium Times Nigeria (2017) “Privatisation of the Power Sector: What Went Wrong?”

- The Advisory Power Team, Office of the Vice President (2015) “Nigeria Power Baseline Report,”

- Nextier Power (2018) “The Aftermath: Unforeseen Contingencies”

- Stillwaters Law Firm (2014) “IFLR1000: Overview of the Nigerian power sector reform”

- Calculated based on the exchange rate as at 14th December 2018: US$1 = N363

- Nextier Power (2018), “The Aftermath: Moving Forward”

This article was first published on Energy for Growth Hub