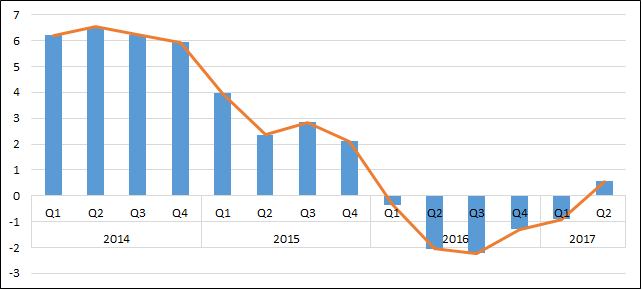

The good news coming out of Nigeria is that the economy has finally exited its worst recession in 29 years. After five quarters of negative growth, the economy grew by 0.55% in the second quarter of 2017, majorly driven by the oil sector which contributed about 78% of the growth recorded (see figure 1). This indicates that the economy is positively responding to the recent improvements in oil prices and domestic oil production.

Figure 1: Real GDP Growth Rate

Source: National Bureau of Statistics, 2017

The recession was initially triggered by an interplay of external and internal factors. On the external side, the crash in global oil prices that became particularly acute towards the end of 2015 led to slowdown in economic growth and depressed the foreign direct investment into the country. The problem was further compounded by renewed restiveness in the Niger Delta in the early 2016, leading to vandalism of major oil and gas infrastructure. This resulted into significant reduction in crude oil production and the foreign exchange earnings for government. These factors reinforce each other to generate substantial shock to the economy leading to the recession in the second quarter of 2016.

The positive growth matches the initial forecast by Center for the Study of Economies of Africa (CSEA) that the impressive but negative economic growths recorded in 2017 Q1 (January-March) suggest the Nigerian economy is on the right track to a positive growth in 2017 Q2 (April-June)[1]. This positive outlook should be sustained for the two remaining quarters in the year, as the key macroeconomic fundamentals (e.g. oil prices, inflation trend, exchange spread among others) look robust, barring any major shock.

For the federal government, which has been criticized for its weak policy response to the initial oil price shock and subsequent exchange rate depreciation that compounded the crisis, the positive outlook reflects an impressive development. In some respects, the government policy intervention especially on the monetary side could be attributed to the positive growth. For example, Central Bank of Nigerian (CBN) has conducted regular mop up operation in the exchange rate market over the past six months. The country has also been able to benefit from the slight oil prices rebound by stemming the pace of crisis in the Niger Delta region. This has resulted in improved stabilization in the exchange rate market as evidence in the reduction in spread between parallel and official exchange rate markets from 42.9% in 2017Q1 to 22% in 2017Q2. In essence, the government initiatives and interventions play a significant role in the positive outlook being experience.

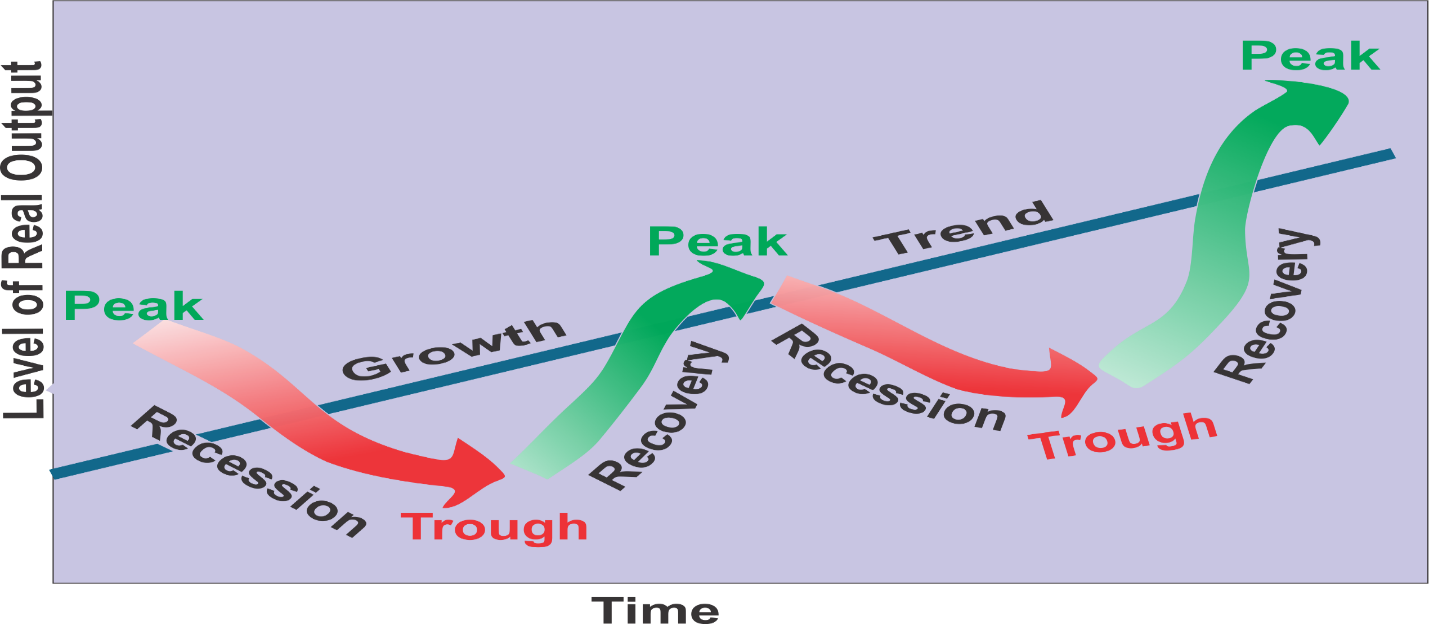

However, it needs to be emphasized that while the country is out of recession, it is not yet out of the woods, as economic recovery is still a long and arduous road ahead. In the economic diction, recession and economic recovery are two distinct phases of business cycles. For instance, based on the definition by the National Bureau of Economic Research (NBER), which officially dates recession in the USA, a recession is defined as a period of significant decline in economic activity spread across the economy, lasting more than a few months, normally visible in production, employment, real income, and other indicators. On the other hand, economic recovery is the phase beginning with the end of a recession until the economy regains and even exceeds peak employment and output levels attained before the decline.

The distinction between the two phases is further demonstrated in Figure 2, where the trend line suggests that a stronger growth rate typically should accompany the economic recovery phase. What this simply means is that Nigeria recession has reached its trough, and economic recovery process has kicked in. However, recent experience of economies affected by global financial crisis of 2008 shows that economic recovery is becoming a much painful process characterized with sclerotic and jobless growth. The case of American economy is a good example in this respect. Many economists still believe that the US economy is yet to complete its recovery process since 2008[2]. A similar outcome is playing out in the Euro zone where the concern around the sclerotic growth has become so huge that a new round of quantitative easing (QE) was implemented in 2015. Some analysts believe the weak recovery process is an emerging feature of the increasing linkages among economies[3]. The extent to which this is true will determine how sustainable and robust the recovery process in Nigeria will be.

Figure 2: Phases of Business Cycle

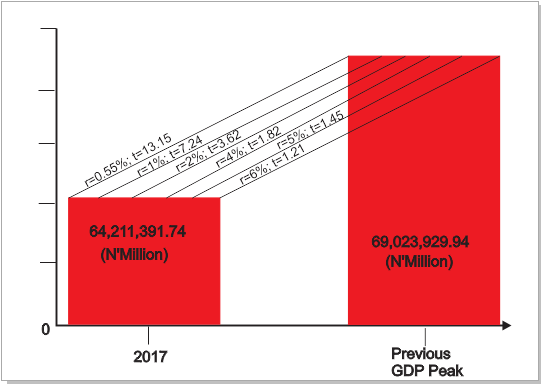

The key point here is that recovery is sometimes harder outcome to achieve than ending a recession. To give a sense of task before the government, we did some basic scenario analysis of growth path and estimated time (t) it will require for the Nigerian economy to return to its initial peak levels of output and growth (r). First, we analyse the different growth trajectories that will be required to get the economy back on track to the recent output peak which was attained in 2015 (see Figure 3). By annualizing the GDP in 2017 and using the present growth rate of 0.55%, the estimate shows that it will take 52 quarters (or 13 years) to regain the loss output. Of course this is somewhat pessimistic, as growth should expectedly pick momentum overtime. At a constant growth rate of 1-2% which is close to most recent IMF projections, the estimated recovery time takes between 3.6 and 7.2 years. Also, assuming a growth rate of about 4-5%, which is close to the government forecast in the Economic Growth and Recovery Plan (ERGP), the recovery takes 1.4 to 1.8years. The best scenario is if the growth returns to its peak period of around 6% achieved between 2012 and 2014. This translates to an expected time of recovery of about 1.2years. Based on this simple analysis, we could expect a recovery period of at least 1.2years. This essentially indicates that a considerable time and efforts lies ahead for economy to fully recover from the effect of recession. This does not discount the fact that other indicators such as employment, poverty reduction, business and consumer confidences need to align.

Figure 3: Scenario 1- Growth Projections toward Recovery

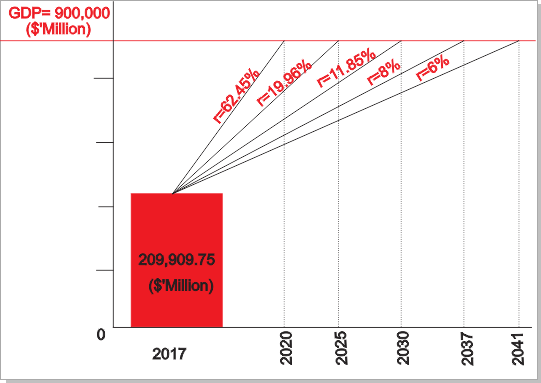

However for a country like Nigeria with enormous developmental challenges and potentials, getting back to its initial output peak represents a mundane goal. In fact, a higher and more ambiguous growth target is required. For example, it is not farfetched to say that Nigerias target of USD900billion GDP as contained in the Vision 20:2020 should be the benchmark. If this is used to simulate the different growth path again, some very fascinating but frightening results emerge. Based on the annualized GDP in 2017, meeting the Vision 20:2020 literally will require an audacious growth rate of 63% per annum. Shifting the target period slightly up to 2025 will require a growth level of about 20% per annum or 12% if 2030 is used as the terminal period. Finally, we simulate with a growth rate target of 6-7% which is historically the peak economic performance recorded in recent years. At this rate, the expected time of reaching the target GDP level will take about 20-24years. A concise summary of these analyses is that an enormous task lies ahead of the government both in terms recovery in the aftermath of the recession and meeting more fundamental developmental objectives of the country. It needs to be added that these growth projections represent mere numbers if it fails to affect poverty, education outcomes, employment, and other development indicators.

Figure 4: Scenario 2- Growth Projections toward Recovery

Given Nigerias economic track record, these growth projections look unachievable, as experience shows recent strong and sustained growth episodes is largely driven by high oil prices. With the recent push into shale oil and renewable energy, such a buoyant outlook for the oil sector seems a thing of the past.

However, larger developmental history shows that this growth trajectory is indeed achievable for developing countries without resource endowment. Recent experiences of two decades of two-digit growth recorded by China is an example. Therefore, policymakers in Nigeria need to search and deeply interrogate the reforms that could help engender a similar growth streak. Overall, reform should begin in these three crucial areas: (1) Structural and institutional reforms of the public sector to ensure better service delivery and improving business-doing conditions; (2) Ensuring political stability and policy consistency, to create an atmosphere for sustained investment and growth; and (3) Formulating a concrete industrialization strategy and ensuring its proactive implementation.

[1] Center for the Study of Economies of Africa (CSEA, 2017), Nigerian Economic Review: First Quarter Report 2017, CSEA, Abuja

[2] http://johnhcochrane.blogspot.com.ng/2015/10/economic-growth.html

[3]http://www.newsmax.com/Finance/StreetTalk/Roubini-economic-globalization-immigration/2014/06/02/id/574648/

Pic Source:Tom Saater/Getty Images