English

English

Arab

Arab

Deutsch

Deutsch

Português

Português

China

China

Tobacco Tax Revenue in Nigeria: To Earmark or Not to Earmark?

Champions of tobacco control both home and abroad have applauded the Nigerian government for its recent approval of higher excise duty on tobacco product. While this duty remains below the standard recommended by the World Health Organization (WHO), it is a step in the right direction. Based on CSEA’s study, the government stands to gain NGN67.7 billion (US$187 million) over a one year period from this new taxation policy. The questions in the minds of people would be: what do citizens stand to gain and how can this additional revenue translate to better well-being for all?

Two possible pathways for welfare gains standout: earmarking tobacco revenue for targeted projects or adding to the pool of government revenue. The CSEA study highlighted that support for tobacco taxation increases by 17 percent if earmarking is introduced, especially among smokers. Most of the respondents view tobacco taxation and earmarking as a means to help smokers quit and improve the wellbeing of citizens. In terms of the wellbeing, respondent prioritize earmarking for public health programmes including treatment of tobacco related diseases, and social programmes for poor households (such as cash transfers). However, with the exception of Ministry of Health, other government parastatals support adding tobacco revenue to the pool of government revenue.

Does it make economic sense to earmark?

Nigeria currently has one of the lowest budget allocations to the health sector. The AU’s Abuja declaration of 2001, stipulates that 15% of the national budget should go to the health sector, but Nigeria only allocates 3.9% of total budget to the health sector in 2018. This implies that government spends a meager sum of N1,888 on each citizen’s health care need for the whole year. This reflects negatively on Nigeria’s health indices; the WHO ranks Nigeria 187th out of 191 countries in terms of health care delivery.

Following the arguments of pro-earmarks, earmarking tobacco revenue ensures a continuous, regular source of funding that are not subject to annual budgetary review. From the CSEA’s stakeholder analysis, 25%-50% of tobacco tax revenue is proposed as the earmarking benchmark. Applying 50% to NGN67.7billion expected revenue would yield an additional NGN33.9billion of earmarked revenue to the health sector over a one-year period. This will result to 9% increase to the sum allocated for citizen’s health care. Similarly, earmarking tobacco taxes can provide a sustainable source of financing for tobacco control. In 2017, about 0.028% of the Federal Ministry of Health budget was allocated for setting up tobacco control unit (TCU) in 2017. However, the TCU received no funds in 2018 due to the ministry’s budget constraints.

Another key argument for earmarking tobacco taxes is to provide an appropriate option for countries where the public financial management (PFM) is weak and policy priorities are not aligned with budget allocations. A major challenge of healthcare financing in Nigeria is the misappropriation of health care funds manifested in the: diversion of drugs and medical supplies, procurement and contract inflation, as well as unethical diversion of budgeted fund among others. While the 2015 National Tobacco Control Act (NTCA) specifies the provision of an earmarked “Fund” for the tobacco control, budgetary allocations of the Ministry of Health have not yet matched this policy priority.

Way Forward

For an earmarking policy to be effective in advancing health and tobacco control priorities in Nigeria, certain considerations need to be made in line with best practices. The prospective policy should:

· Have a clear expenditure purpose that is neither too narrow nor broad:

The expenditure purpose should be narrow enough to link funds clearly to activities and results in order to advance health sector priorities. However, it ought not to be too narrow to introduce excessive rigidities or economic distortion. Philippines, South Africa, Vietnam and Estonia provide notable examples of this.

· Have a strong but flexible revenue-expenditure link to avoid unhealthy dependence:

Neither should the program/unit for earmarking be totally dependent on the earmarked funds without other sources of revenue, nor should the expenditure needs of the program/unit determine the tax rate. On one hand, earmarked revenue is seen to be completely driving expenditure in Ghana: earmarked VAT and social security contributions accounts for 90% of revenues for National Health Insurance Scheme (NHIS) in Ghana. On the other hand, the Estonia Health Insurance Fund (EHIF) expenditure has been completely driving the pay roll tax revenue proportions earmarked for EHIF. Hence, when revenue from payroll tax contributions became insufficient to cover expenses in 2013, policymakers set to broaden the revenue base to address the structural deficit.

· Be a “Soft” earmark with option for reallocating funds to emerging priorities:

To foster tobacco control, an earmarked fund can be dedicated to the TCU within the Federal Ministry of Health, with a reserve fund that allows funds to be reallocated to new priorities within the health sector as they arise.

· Incorporate a strong PFM and governance systems for monitoring and reporting the revenue flows and impact:

The PFM and governance systems should incorporate reporting systems at different levels to help improve transparency and accountability.

· Have a clear medium-term time horizon for earmarking review:

A prospective tobacco tax earmarking policy should incorporate a timeframe for review and impact assessment. This should possibly be in line with the Medium-Term Expenditure Framework to give time for the policy effect to crystalize.

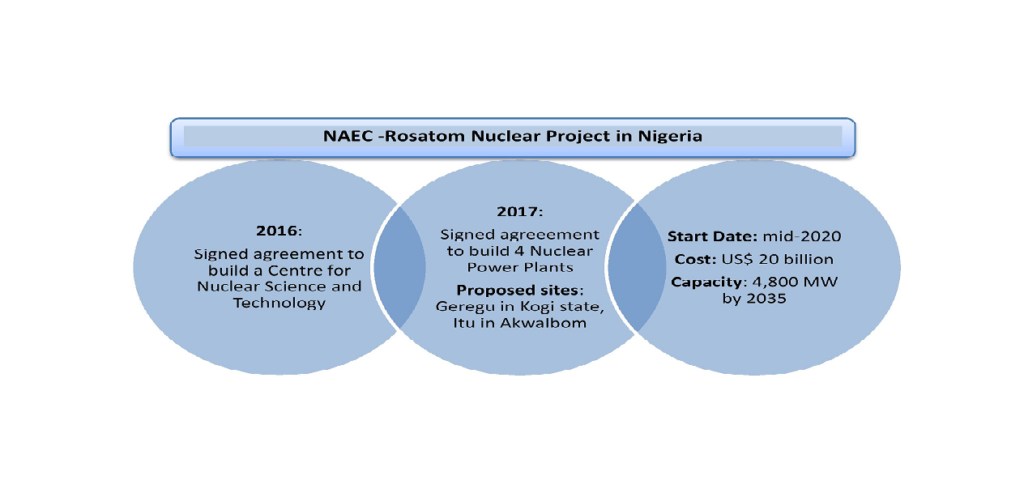

In light of the nuclear power development, two key questions call for objective analysis:

In light of the nuclear power development, two key questions call for objective analysis:

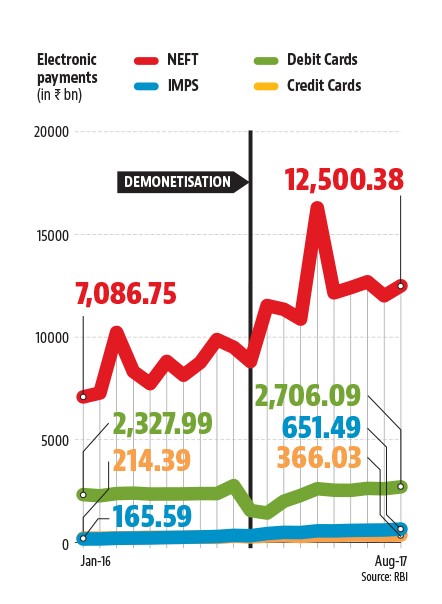

Source: mbauniverse, 2018

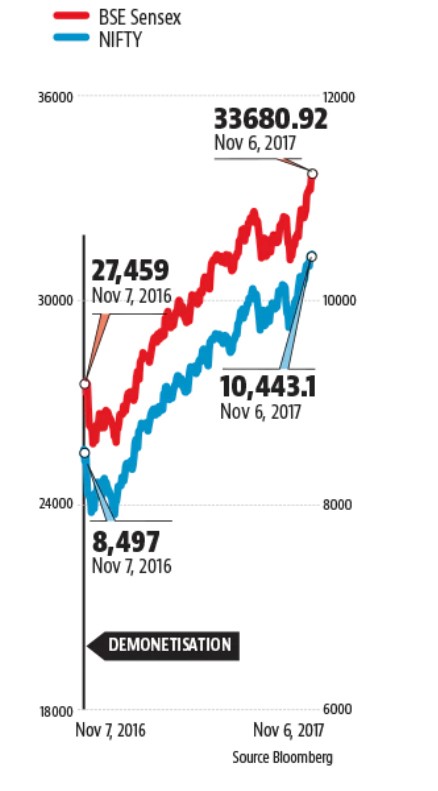

Source: mbauniverse, 2018