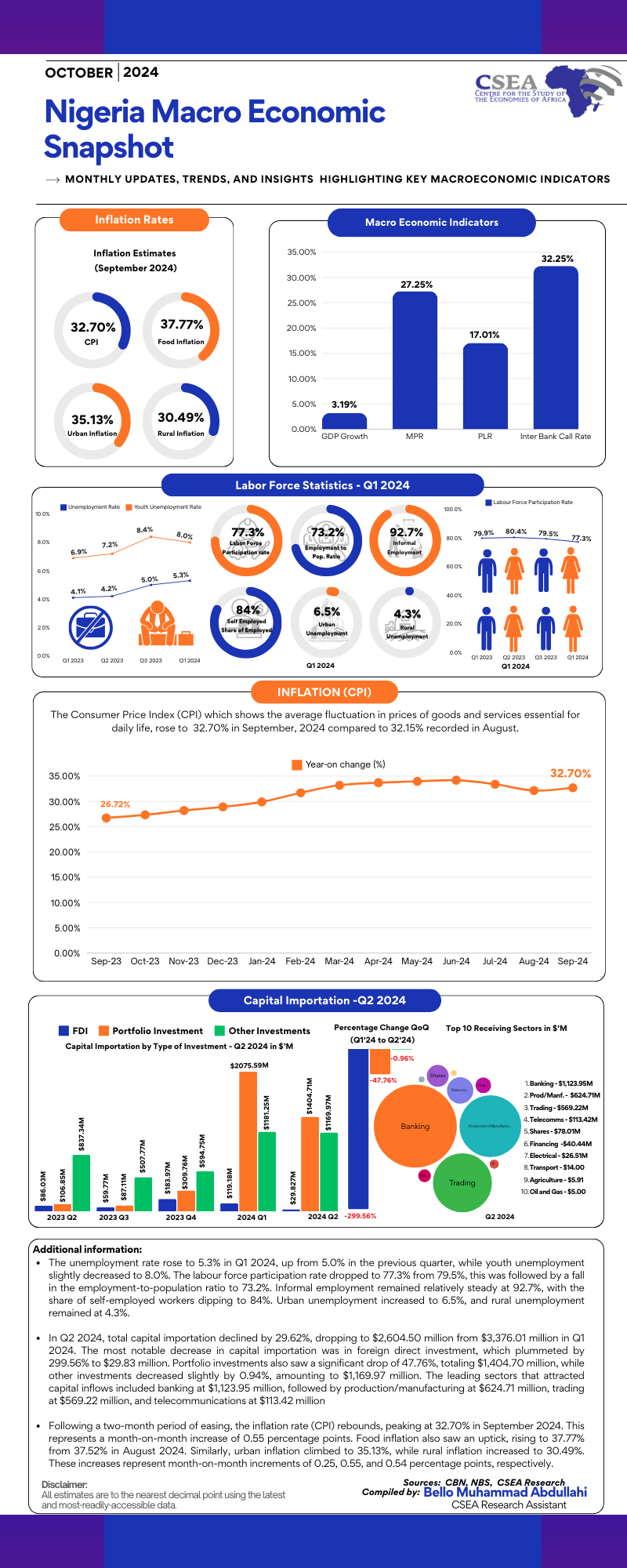

According to the National Bureau of Statistics (NBS), Nigeria's total goods trade stood at ₦31,892.46 billion in Q2 2024, down 3.76% from the previous quarter but up 150.39% from the number reported in Q2 2023. Exports accounted for 60.89% of overall trade, worth ₦19,418.93 billion. Nigeria's export trade was dominated by crude oil (₦14,559.56 billion), accounting for 74.98% of total trade, followed by agricultural goods (₦973.69 billion), raw materials (₦366.91 billion), solid minerals (₦58.56 billion) and manufactured goods (₦480.82 billion). Total imports accounted for 39.11% of total commerce in Q2 2024, totaling ₦12,473.53 billion, a 10.71% decline from Q1 2024. Mineral fuels were the most popular import category, followed by machinery and transportation equipment, chemicals, and allied items, which accounted for 35.40%, 23.08% and 15.12% of total imports respectively. While a decrease in imports may help reduce trade deficits and highlight Nigeria's improving export strength relative to import demand, it also implies slower economic activity or limited access to vital imports such as machinery and transportation equipment. Furthermore, Nigeria's strong reliance on oil exports, which account for nearly 75% of total commerce, indicates that the country's trade performance is extremely vulnerable to global oil price swings, and demand changes. The government must devote its attention to diversification policies that will improve the contribution of non-oil sectors to Nigeria's export base such as agriculture, raw materials, solid minerals and manufactured goods to promote economic stability and resilience to external shocks.

Read More

Download PDF

English

English

Arab

Arab

Deutsch

Deutsch

Português

Português

China

China